With passage of the new Blended Retirement System (BRS) in 2016, the Defense Department's Office of Actuary, assisted by computer modeling from the think tank Rand Corp., made some assumptions critical to planning future military retirement cost obligations.

More than 862,000 active-duty members and 202,000 drilling Reserve and National Guard personnel, actuaries forecast, would opt to leave their High-3 retirement plan for the BRS during a year-long "open season" that ended Dec. 31.

Turns out those projections were far too high.

Near-final tallies of opt-in decisions for BRS (through Dec. 17) show only 280,000 active-duty members and just over 72,000 reserve component personnel chose to shift out of the High-3 plan.

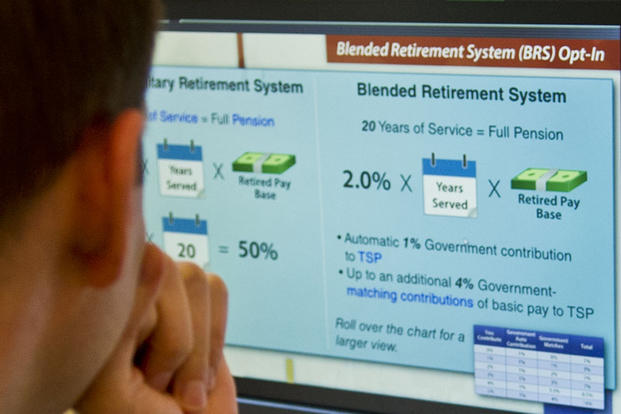

High-3 is the more generous retirement plan for members who serve 20 years or more and earn its lifetime annuity. The BRS provides a 20 percent smaller annuity. But for the majority of service members who don't serve full-length careers, the BRS also provides a Thrift Savings Plan that is bolstered by government matching of member contributions.

Assuming no extraordinary rush to switch plans in its final two weeks of the open season -- before and after Christmas -- the BRS opt-in results fell as much as two-thirds below projections for active-duty and reserve component forces.

In July 2016, the Department of Defense Board of Actuaries, which is responsible for ensuring the DoD Military Retirement Fund is properly valued and actuarially sound, accepted Rand's estimate that a total of 916,754 active and reserve component members would opt into the BRS when it became available.

At the same time, the board concluded future military retirement obligations for the department could be lowered by 2.9 percent for the active force and .8 percent for reserve components, given the lower annuity formula for the BRS.

DoD actuaries re-examined their estimates last year and raised the opt-in total by more than 100,000, to predict that 1.06 million active and reserve component members would choose to shift to the BRS during the open season.

The opportunity to switch plans was opened to more than half of all active-duty and reserve component members. Active-duty members could switch if they had fewer than 12 years in as of Dec. 31, 2017. Reserve component members could do so if they had fewer than 4,320 drill points for retirement by that date.

Members who enter service on or after Jan. 1, 2018, have no choice; BRS became their plan. Active-duty members who had more 12 years, and reservists with more than 4320 retirement points, by Dec. 31, 2017, stayed under High-3.

The BRS is called "blended" because it combines an immediate but smaller annuity after 20 or more years with a Thrift Savings Plan enhanced by government matching of member contributions. That 401(k)-like nest egg can be rolled into a civilian employer's 401(k) benefit upon leaving service.

Only 49 percent of new officers and 17 percent of enlistees attain 20 years of active-duty service to be able to retire. Because enhanced Thrift Savings helps that majority who leave short of retirement eligibility, the BRS was expected to be a more popular option, particularly for enlisted members in their first or second enlistment and for officers completing initial service obligations.

DoD actuaries predicted in their Military Valuation Report that the vast majority of active-duty officers and enlisted with fewer than 12 years of service would opt into the BRS. Their opt-in assumption for active-duty members with one year of service, for example, was 85.5 percent for officers and 95 percent for enlisted. Only for enlisted members past their 9th year of service, and for officers past the 10th year, did assumed opt-in rates fall below 50 percent.

The blended retirement has two more unique features. There's a one-time "continuation payment" payable by the 12th year of service, to be set at a minimum equal to two-and-half months of basic for active-duty members who agree to serve four more years. The minimum is one-half month of active-duty pay for reserve component personnel who make the same deal.

Also, the BRS allows those who reach retirement to receive in a lump sum of either 25 percent or 50 percent of the value of annuities payable until old age. The lump sum is designed to help a member buy a home, start a business or pay off debts in return for cutting his or her annuity by one-quarter or half until age 67.

Actuarial groups have railed against the lump-sum offer as an unfair choice for members who retire under the BRS, given the amount they would forfeit in total future benefits for the enticement of many thousands of dollars in cash.

Whatever the reasons, the BRS features didn't attract nearly the number of current force members that the actuaries and Rand computer modeling forecast.

Through mid-December only 21.6 percent of active-duty soldiers eligible for the BRS switched from High-3, giving the Army the lowest opt-in rate of the four DoD military branches. The active-duty opt-in rate was 26.3 percent for the Air Force, 28.3 percent for the Navy, and a surprising 53.7 percent for the Marine Corps.

The BRS likely was far more attractive to Marines because the Corps keeps its career force proportionally smaller than do other service branches. A higher percentage of Marines can serve only a tour or two before returning to civilian life. With the BRS, they will leave with heftier Thrift Savings Plan balances.

The Marine Corps Reserve also had a higher opt-in rate to the BRS, at 37.6 percent compared to 8.4 percent for eligible Army National Guard members, 9.4 percent for the Army Reserve, 10.1 percent for the Navy Reserve, 10.3 percent for the Air Force Reserve, and 10.6 percent among eligible Air National Guard members.

The BRS opt-in rates for active-duty forces across the DoD was 29.2 percent through mid-December and 10.6 percent for reserve component forces. Those were far lower than anticipated. In fairness, the Defense Board of Actuaries, at the time it embraced Rand's modeling estimates, said it did so reluctantly, concluding that "we have no better basis for projecting opt-in behavior."

In addition to those members who voluntarily opted into the BRS during the open season, more than 142,000 enlisted recruits and officers who first entered service in 2018 automatically became part of the BRS generation.

To comment, write Military Update, P.O. Box 231111, Centreville, VA, 20120 or email milupdate@aol.com or twitter: @Military_Update.

")

")

")

")

and the Inflation Reduction Act of 2022 at the U.S. Capitol on Wednesday, Oct. 8, 2025, in Washington. (John McDonnell/AP Photo)")

questions U.S. Attorney General Pam Bondi as she testifies before the Senate Judiciary Committee in the Hart Senate Office Building on Capitol Hill on Oct. 7, 2025, in Washington, D.C. (Alex Wong/Getty Images/TNS)")

.")

.")

")

")

-United States Defence Ministers' High Tea, as part of the ASEAN Defense Ministers' meeting, in Kuala Lumpur, Malaysia, Saturday, Nov. 1, 2025. (Hasnoor Hussainl/Pool Photo via AP)")